Global markets -

What the tenpin bowling bubble teaches us about AI

Technological improvements sparked a bowling boom in the US in the late 1950s. But after growth stalled, the pastime never recovered to its former glory. With investors showing feverish interest in AI, Jason Da Silva, Director, Investment Strategy, explains the lessons they should learn from the bowling bubble.

As long as there have been financial markets, there have been asset bubble manias. We continue to get questions from clients on whether the surging market values of companies investing in artificial intelligence (AI) signal the next bubble. The surprising case of a bubble in tenpin bowling illustrates the key factors investors should watch.

The bowling boom: A cautionary tale

Technological innovation often fuels asset bubbles by driving rapid growth and speculation. In tenpin bowling, the late-1940s introduction of the automatic pinsetter cut labour costs and enabled 24-hour operations, making the sport more accessible.

This sparked an investment boom into the sport: US bowling alleys nearly doubled from 6,600 in 1955 to 12,000 by 1963. Investor enthusiasm followed — Brunswick Corporation’s stock (a bowling alley equipment maker) rose 16-fold between 1957 and 1961.

But by the mid-1960s, growth stalled and profitability waned. The industry had overbuilt and misjudged long-term demand. Many alleys were financed by equipment makers like Brunswick, whose stock plunged from $75 to $13 in a year as loans soured. Competing leisure options further eroded demand. Today the number of US bowling alleys is less than a third of the 1963 peak.

Enter artificial intelligence

So how does this relate to the current excitement around AI?

We are in the early stages of a significant technological shift. AI’s capabilities are real, and progress is happening fast. Unlike bowling — a consumer trend with natural limits — AI is a foundational technology with broad cross-sector potential. Businesses are already reporting measurable productivity gains, and leading AI companies are showing real earnings growth to support strong share price movement. Nvidia revenue surged 69% year-on-year in the first quarter of 2025 to $44bn and OpenAI recently announced revenues of $10bn in early 2025, up from $5.5bn in December 2024.

That said, the risk of excess remains. Capital is pouring into chips, data centres, and startups, and parts of the ecosystem could expand too aggressively. If growth expectations are not met, these investments may face a painful reset.

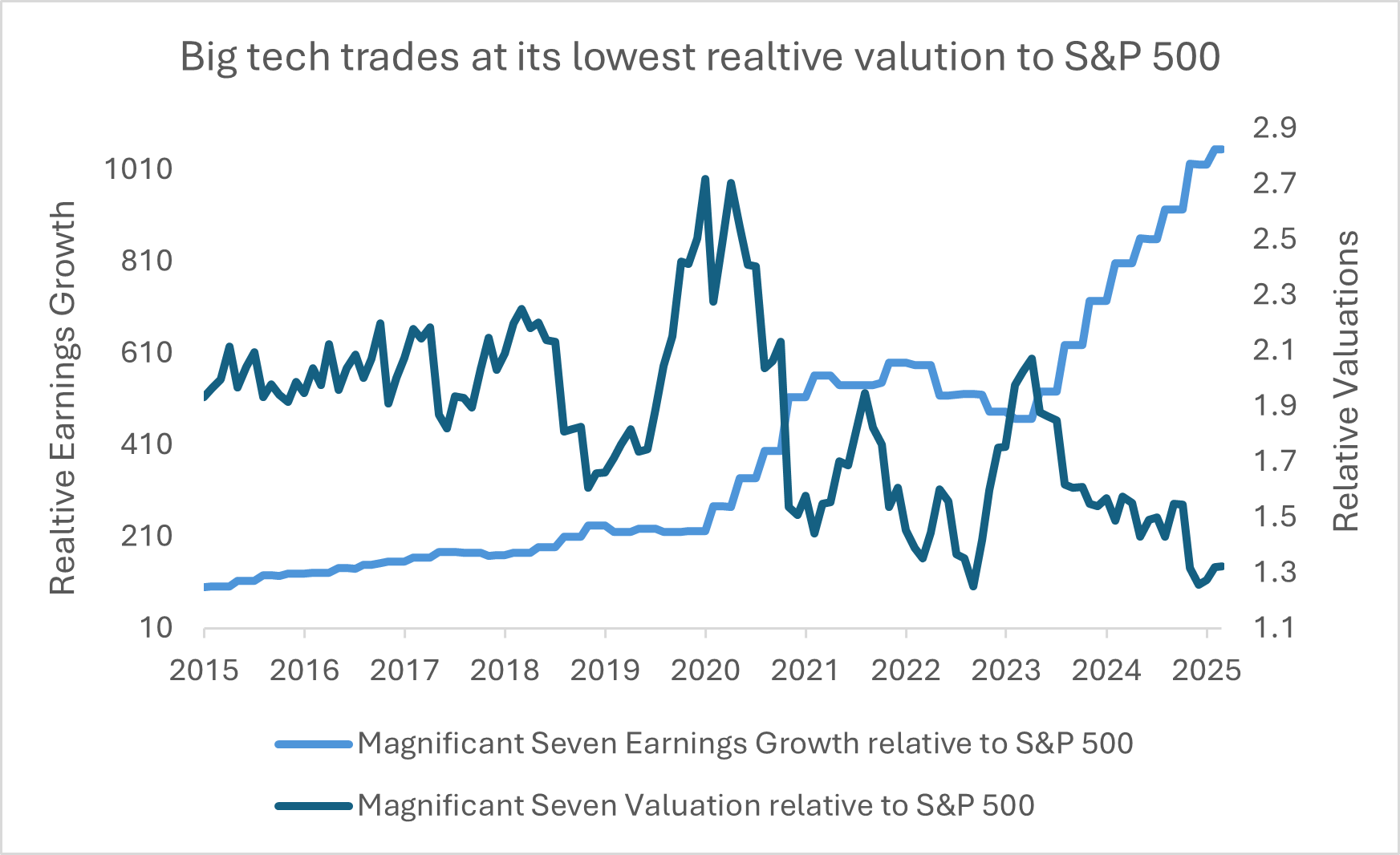

Valuation discipline is also critical. The bowling bubble showed how prices can decouple from fundamentals. In AI, valuations are varied – some stocks do show signs of bubble-like pricing. However, where much of our client capital is concentrated — in large, diversified tech firms — valuations are not obviously excessive relative to earnings strength and balance sheet quality.

Key lessons for investors

Real innovation can still attract unrealistic expectations

The automatic pinsetter genuinely transformed bowling. But growth projections still overshot. With AI, the technology is real but expectations must be grounded.

Watch for overcapacity and capital misallocation

In the 1960s, too many alleys were built too quickly. Today, it is data centres, AI chips, and startups, some of which may never generate sustainable returns. Focus on firms with clear differentiation and competitive moats.

Valuation discipline

Some AI stocks show stretched multiples untethered to fundamentals. Prioritise businesses with realistic paths to profitability and sustainable margins. Avoid those driven purely by narrative.

How Arbuthnot Latham has invested in AI

Our investment management team has been keeping a close eye on the AI sector over the past few years. They believe quality companies still have room to grow and to give our clients exposure to this potential they took a position in a semiconductor ETF and steadily increased exposure to the tech-majors as leaders in the sector.

During the market turmoil in early 2025 they added to both positions when prices dipped.

To understand the opportunities and risks in AI, our team conducts regular deep dive research, including consulting with fund managers with expertise in the field and experienced individuals in the AI space.

We approach AI with a balanced perspective, recognising both its transformative potential and the risks of speculative excess. The AI market is not destined to collapse like the bowling industry, but its trajectory depends on whether significant investment today translates into durable returns in the future.

History does not repeat, but it often rhymes. By drawing lessons from past bubbles, investors can better navigate both the opportunities — and the pitfalls — of AI.

Find out more about our wealth management and investment management services.

Latest insights

Read more

Subscribe to our latest insights

Sign up to receive insights from our experts and partners, giving you fresh ideas and different perspectives on topics that help you go further. Plus, get exclusive invites to events and webinars.

Author -

Jason Da Silva

Director, Global Investment Strategy

Jason Da Silva joined Arbuthnot Latham in 2022, as a senior research analyst and in 2023 he was promoted to Director, Global Investment Strategy. He most recently spent four years at boutique asset manager Obsidian Capital focused on direct equities, fixed income, commodities, and currencies. Previously, he worked at EY, where he became a Chartered Accountant before rotating into the EY corporate finance division. Jason holds both a CA(SA) and a CFA.

DISCLAIMER

This communication should be considered a marketing communication. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research. It is for information purposes only and does not constitute advice, a solicitation, recommendation or an offer to buy or sell any security or other investment or banking product or service. You should seek professional advice before making any investment decision. The value of investments, and the income from them can fall as well as rise, and may be affected by exchange rate fluctuations. Investors could get back less than they invest. Past performance is not a reliable indicator of future results. The tax treatment of investments depends upon individual circumstances and may be subject to change.

The contents of this communication are based on opinions or conditions as at the date of writing and may change without notice. To the extent permitted by law or regulation, no warranty of accuracy or completeness of this information is given and no liability is accepted for its use or reliance on it.