Global markets -

Quarterly market update: Dollar weakness, resilient growth, AI, and how we are adapting investments

Find out how our investment team are reacting to the recent themes they have identified, including: headwinds for the dollar, AI investment, and inflationary pressures.

Video -

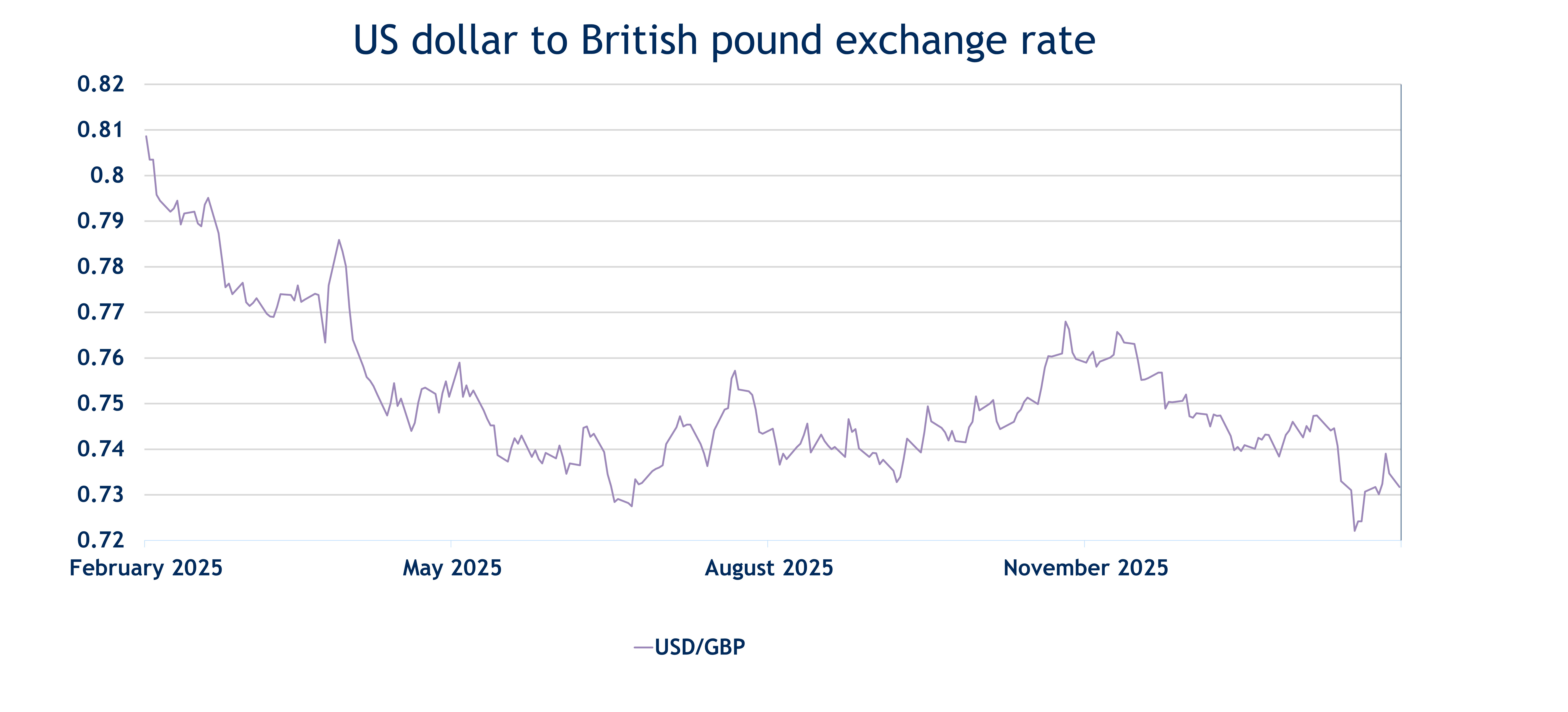

Dollar weakness

We expect the US dollar to weaken in 2026. Valuations remain at multi‑decade highs, creating a headwind for further strength. Although US growth should stay robust, we anticipate stronger momentum from other regions, supporting non‑dollar currencies. A softer dollar would also create a more favourable environment for non‑US equities, which often outperform when the dollar loses momentum.

Our response: We have positioned portfolios to both protect clients from dollar weakness and to capitalise on opportunities that may result from this softening. Dollar weakness will be a headwind for our US equity allocation, and we have reduced our positioning further. A softer dollar historically boosts performance in Emerging Markets, and so we have added to this region. We also expect Emerging Markets equities to benefit from rising global investment in AI technologies, as many Emerging Market economies are large exporters of the key components in the AI value chain. In addition, we added to Emerging Market debt within our fixed income allocation. Not only does Emerging Market debt offer attractive yields, we also expect strengthening local currencies to add to the total return of this asset class.

Expectations for industrial production

Resilient global growth – underpinned by sustained AI-driven investment and fiscal easing – is set to lift global industrial production. This environment provides a constructive backdrop for the cyclical sector of the global economy and demand for commodities.

Our response: In addition to increasing our exposure to Emerging Markets equities, which tend to do well when global growth is expanding, we also initiated positions in the global materials and industrials sectors. Both sectors tend to outperform during periods of expanding industrial production, and we see several catalysts supporting this trend. The accelerating buildout of AI-related infrastructure continues to drive demand for industrial equipment and critical raw materials. At the same time, an improving backdrop for global growth further reinforces the outlook for these cyclical sectors.

Moreover, materials and industrials typically benefit from a weaker US dollar, which enhances global demand and improves the backdrop for non-US producers. This dynamic aligns closely with our broader positioning theme around the weaker US dollar.

Within our US allocation we shifted investments to smaller companies, which will do well in a cyclical environment, and we adjusted our EU allocation to increase exposure to cyclical sectors such as financials and industrials.

Inflationary pressures

Stronger global growth raises the risk of renewed inflation pressure just as central banks step back after months of easing. Constructive growth and ongoing fiscal support keeps yields elevated, limiting upside for bond performance.

Our response: We have trimmed our government bond exposure in favour of global equities, taking on a modest increase in risk given the solid growth outlook. Furthermore, in the short term, we expect sticky global inflation will continue to be a headwind for government bonds. Within our government bond allocation, we maintained the position in UK bonds, as the macro-outlook for the UK continues to differ from other major economies. We expect softer economic growth in the region to keep inflation pressures down, which should allow the Bank of England to take a more flexible, supportive approach to interest rates.

We have a positive outlook for AI

We have a positive outlook for AI, as large technology companies continue to ramp up capital expenditure to stay ahead in the AI buildout. We favour areas best positioned to monetise this surge in spending, particularly semiconductors.

Our response: Our exposure to US equities remains overweight to large-cap technology sectors, as these companies continue to demonstrate strong fundamentals and remain at the forefront of AI innovation. Their expanding capital expenditure underscores their leadership in the ongoing tech investment cycle.

We also increased our allocation to semiconductors, which stand to benefit most directly from rising AI related investment and the broader demand for advanced computing infrastructure.

Balance and resilience

Despite a broadly supportive macro backdrop, risks persist across markets, particularly equity valuations, and we believe maintaining a well-diversified portfolio remains crucial. We therefore continue to hold positions that provide balance and resilience across different market environments.

Our response: We increased our allocation to hedge funds, focusing on merger arbitrage and convertible bond arbitrage strategies. Both offer strong potential returns with better downside protection relative to corporate bonds, where we see the risk return profile as unattractive due to high valuations.

We also added to catastrophe bonds, which remain a strong diversifier given their low correlation with political, economic, and market events.

Lastly, we increased our gold allocation to further strengthen diversification across the portfolio.

Latest insights

Read more

Author -

Jason Da Silva

Director, Global Investment Strategy

Jason Da Silva joined Arbuthnot Latham in 2022, as a senior research analyst and in 2023 he was promoted to Director, Global Investment Strategy. He most recently spent four years at boutique asset manager Obsidian Capital focused on direct equities, fixed income, commodities, and currencies. Previously, he worked at EY, where he became a Chartered Accountant before rotating into the EY corporate finance division. Jason holds both a CA(SA) and a CFA.